How do VCs invest?

Early stage investing is much simpler than early-stage company building.

A founder has no option value, they are dealt one hand and must make it work.

Investors see many hands and have the luxury of waiting to bet big for the right set of cards.

This means investors evaluate companies in parallel, not sequentially. Every investor is benchmarking new companies with the previous 1 to N companies they have seen before or are currently looking at.

So, what are they looking for?

I believe there are four simple things.

(1) Will people want the unit of value ?

(2) Can they distribute this value efficiently & at scale to those people?

(3) Are there enough people who want it to make $100M+ revenue?

(4) Is the value proposition greater than incumbents and will this hold true in the future?

Yes x4 = Maybe…

A bakery would pass (1) but fail (2).

A marketplace for collectable stamps would pass (1) & (2) but fail (3).

A new crypto exchange would pass (1) & (2) & (3) but probably fail at (4).

A B2B SaaS company with breakthrough tech may pass all of them.

BUT even if it’s a YES to all FOUR, it’s just table stakes, the company is still compared to all the other companies that VC has seen. They are thinking about which has the highest probability of achieving all four.

You might think that I have missed something — what about the importance of the founders?

Founders are so important that they are baked into every question. Can they build something people want? Can they sell it? Can they see a path to new markets? Can they beat their competition?

In fact, the VCs will even go against these requirements and invest in real estate businesses that don’t scale when the founders are seemingly incredible, or appear to be, like in the case of WeWork.

Here is the process:

Will people want the unit of value it creates?

What is the unit of value that the product creates? Does it save time or money, create revenue, create status, etc.? Once this is clear, we identify the target customer and try to sample consensus.

VC: Would you pay for something that could save 8 hours of time?

Target Customer: Probably not, it only takes us to 1 or 2 hours to do that anyway.

For B2B, this easy, all businesses want to save time and money. Customer calls are great.

For B2C, this is hard, because who knew humans would pay for Cryptopunks? It’s easier to wait for some traction and data or look at forums, reviews or surveys of what people want.

Can they distribute this value efficiently & at scale to those people?

It has been said venture capital is the business of turning an ember into a forest fire. But not all kindling burns equally.

Great product companies routinely die because the team can’t sell or scale the product.

For sales efficiency, it’s all about having some form of go-to-market advantage. Tech is hyper-competitive, there are thousands of software companies in each category. There needs to be a way to stand out.

VCs will look at your LTV/CAC and CAC payback as this will usually reveal whether there is some inherent advantage in selling.

For scalability, this question is far easier. Is the business pure play software? It scales. Anything else — we are more cautious and look at the gross margins. Generally, we are looking for 60%+ margins or a path to it.

Are there enough people who want it to make $100M+ revenue?

The fun part, market sizing.

A lot of founders get frustrated that VCs are looking for businesses that can make more than $100M of revenue within a market. Isn’t it still a great business if it makes $20M?

Certainly. But venture is governed by power laws — all returns come from a few companies. If a business only has a path to $10M in revenue, the VC is taking the same level of risk as any other high-risk startup but are greatly capping their upside — and the data shows this is where all the returns come from.

We are looking for large expanding markets where there is a clear path to $100M in revenue if the business takes a % of the market.

Everyone will say their market is a billion or trillion dollar market. Usually, this is not true.

We calculate the market size both top down and bottom up.

Top down = Using secondary research to find market than assuming a percentage

Bottom up = Price x Quantity (find number of potential customers using statistics)

For bottom up, there are a few tricks we can use to get the statistics:

- Use FB consensus tool to figure out how many people are in the target market persona

- Use public statistics e.g. 100,000 SMEs in North America in Construction x Price

- Use SEMRUSH to see web traffic of incumbents

- Use public filings to calculate revenue for public company incumbents

- Get creative (we have even used Steam Gaming data to calculate market size for a hardware company)

We are also trying to understand the tailwinds at play that are dramatically changing the size of the market in the oncoming years.

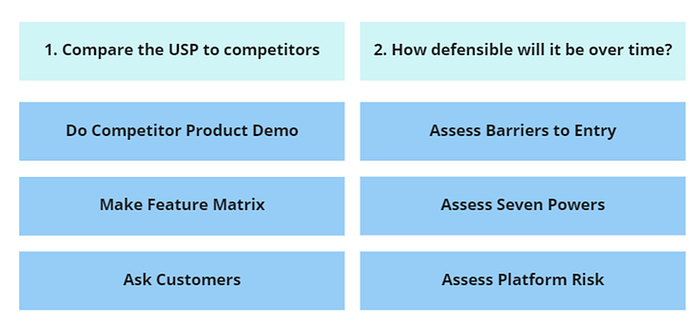

Is the value proposition greater than incumbents and will this hold true in the future?

The final step. Customers want it, the business can sell, and it scales, the market is huge. But if there is no differentiation or barriers to entry, a large market will get competed away and the business will not be large enough for venture scale.

We try and compare the unique selling proposition for the business to what’s on market. It involves understanding the 2–3 things customers actually care about.

We then do our own side by side feature matrix and see if the company is 10x better to what’s on market for the things that matter to them. The art of this part of the process is knowing what to disregard in the startup’s competitor matrix.

Most of the time the features that are listed aren’t really a make or break for customers.

Then we think about how defensible this advantage will be over time. There are some great articles to read on this topic.

And that’s it!

At any given time an investor is looking at 10-30 companies, and they are comparing each with which has the highest chance of achieving all four.

It’s an imperfect process. But I hope this article has helped lift the veil of secrecy in the decision-making process for investing in early-stage startups.